All other depreciating assets require a useful life estimate.

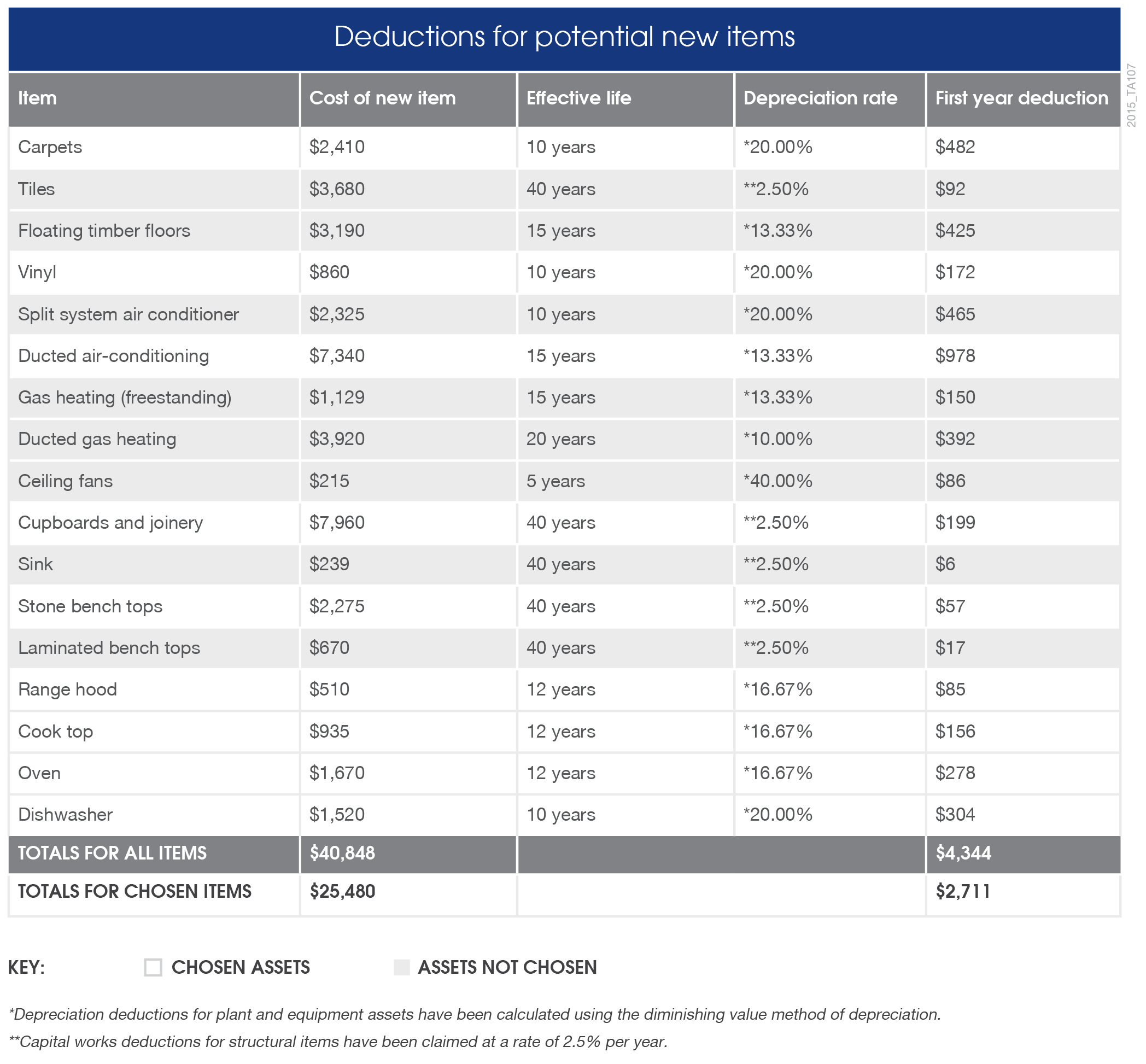

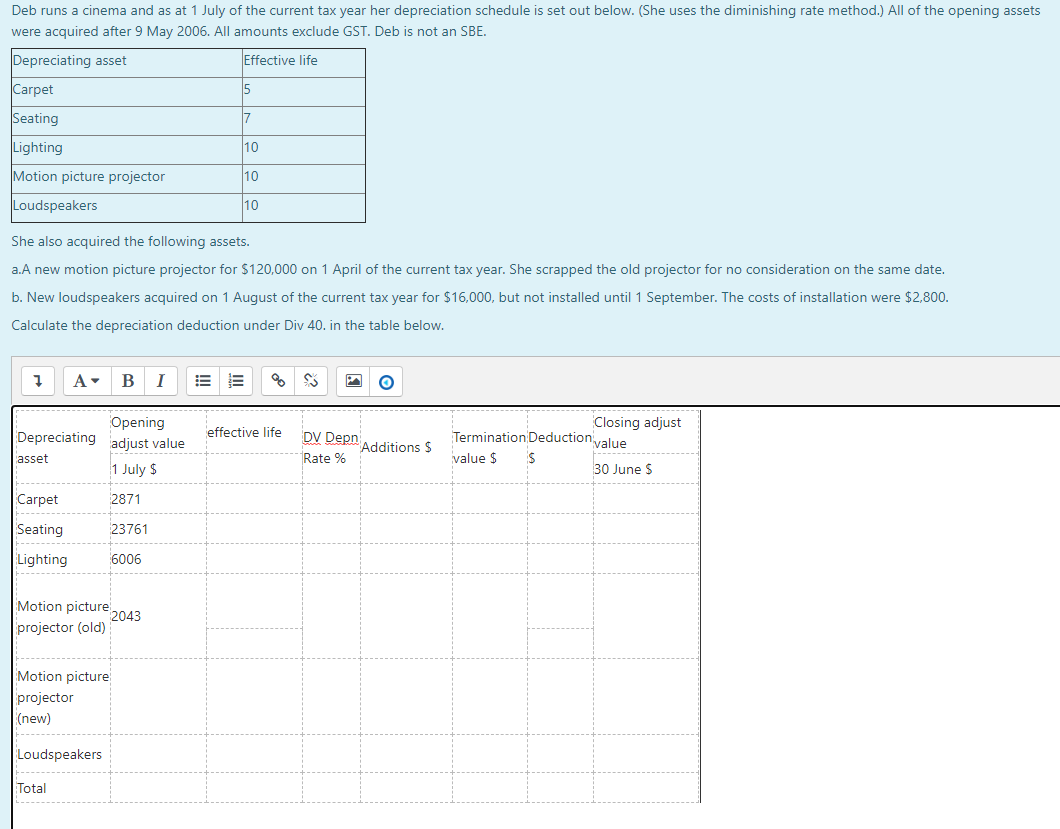

Carpet depreciation rate.

If you decide to replace carpets before the ten year effective life is complete be aware that any remaining depreciable value can be claimed as scrapping.

A deduction for any vehicle if the deduction is reported on a form other than schedule c form 1040 or 1040 sr.

This applies however only to carpets that are tacked down.

Depreciation for property placed in service during the current year.

See chapter 5 for information on listed property.

Depreciation commences as soon as the property is placed in service or.

10 years depreciation charge 1 000 10.

Rental property owners use depreciation to deduct the the purchase price and improvement costs from your tax returns.

We set depreciation rates based on the cost and useful life of assets.

Manufacturing 11110 to 25990.

Original cost of carpet.

Carpet life years remaining.

Depreciation on any vehicle or other listed property regardless of when it was placed in service.

Like appliance depreciation carpets are normally depreciated over 5 years.

The prescribed depreciation methods for rental real estate aren t accelerated so the depreciation deduction isn t adjusted for the amt.

10 years 8 years.

The landlord should properly charge only 200 for the two years worth of life use that would have remained if the tenant had not damaged the carpet.

Textile leather clothing and footwear manufacturing 13110 to 13520.

However accelerated methods are generally used for other property connected with rental activities for example appliances and wall to wall carpeting.

Repairing is the key to your tax treatment replacing destroyed appliances carpet and linoleum are an asset and depreciated 5 years.

100 per year age of carpet.

Diminishing value rate prime cost rate date of application.

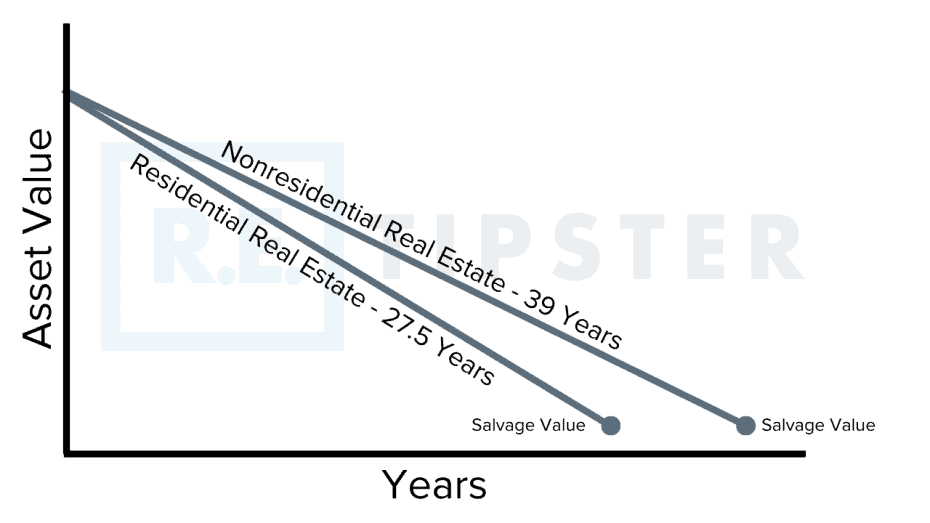

If the carpet is glued down perhaps in a basement then it becomes attached to the property and must be depreciated over 27 5 years.

Depreciation rates are based generally on the effective life of an asset unless a write off rate is prescribed for some other purpose such as the small business incentives.

Depreciation on buildings depreciation was allowed on most buildings until 2010 and for the 2012 2020 income years the depreciation rate for buildings with an estimated life of more than 50 years was set at zero.

How long an asset is considered to last its useful life determines the rate for deducting part of the cost each year.

Beamers including warpers 15 years.

Depreciation rates assets are depreciated at different rates.